Add or remove VAT, extract VAT from inclusive prices, and total Net, VAT and Gross across multiple lines. Preset 2026 rates for the UK, EU and 37 countries.

Have feedback? Report bugs, suggest features, or share your thoughts — we read them all

What is VAT?

VAT (Value Added Tax) is a multi-stage consumption tax applied to the value added at each step of production and distribution. Businesses charge VAT on sales (output VAT), reclaim VAT paid on business purchases (input VAT), and remit the difference to the government — so the cumulative tax burden ultimately falls on the final consumer. Over 170 countries use a VAT or VAT-equivalent system (GST in Commonwealth countries), making it the most common consumption-tax model globally.

Two operations matter day-to-day: ADDING VAT when you have a net price and need the gross customer-facing total, and REMOVING VAT when you have a VAT-inclusive receipt and need to extract the tax for input-VAT reclaims or expense reports. This calculator does both, with current 2026 rates pre-loaded for 37 major economies — including the UK (20%), Germany (19%), France (20%), Spain (21%), Finland (25.5% since Sept 2024), Greece (24%), Turkey (20% since July 2023), Israel (18% since Jan 2025), Singapore (9% since Jan 2024) and UAE (5%).

VAT Calculation Formulas

Two operations, two formulas — the second is the inverse of the first:

Finland: 25.5% standard (raised from 24% on 1 September 2024)

Greece: 24% standard, 13%, 6% reduced

Ireland: 23% standard, 13.5%, 9%, 4.8% reduced

Turkey: 20% standard (raised from 18% on 10 July 2023)

Israel: 18% standard (raised from 17% on 1 January 2025)

Russia: 20% standard (raised from 18% on 1 Jan 2019)

United Arab Emirates: 5% (introduced 2018)

Singapore: 9% (raised from 8% on 1 Jan 2024 — second hike in 12 months)

Australia: 10% GST

New Zealand: 15% GST

India: 5%, 12%, 18%, 28% (four-slab GST since 2017)

Types of VAT Treatment

Standard Rate: applied to most goods and services — the headline rate

Reduced Rate: lower rate for essentials such as food, books, children's items, public transport

Zero Rate: 0% VAT charged but supplier CAN reclaim input VAT (exports, some basic foods)

Exempt: 0% VAT charged but supplier CANNOT reclaim input VAT (financial services, healthcare, education in most countries)

Out of Scope: not VAT-able at all (wages, donations, dividends, sale of going concerns)

For Business Owners

Register for VAT when you cross your country's threshold — UK £90,000 since April 2024, Germany €25,000, Ireland €40,000-€80,000 (different for goods vs services)

Voluntary registration below threshold can pay off if most inputs carry reclaimable VAT — common for B2B service businesses

Issue compliant VAT invoices: your VAT number, customer's VAT number for cross-border B2B, VAT amount as a separate line, rate, net and gross totals

Submit VAT returns on time — UK quarterly via Making Tax Digital, EU monthly or quarterly depending on size, with daily penalty interest after deadline

Keep VAT records 5-10 years depending on jurisdiction (UK 6, Germany 10, Ireland 6)

Track exempt vs zero-rated supplies separately — both have 0% output but only zero-rated allows full input reclaim

For cross-border B2B services in the EU, use reverse charge: the buyer self-accounts for VAT, you charge 0%

Use the OSS (One-Stop Shop) scheme to declare EU-wide B2C sales centrally instead of registering in every member state

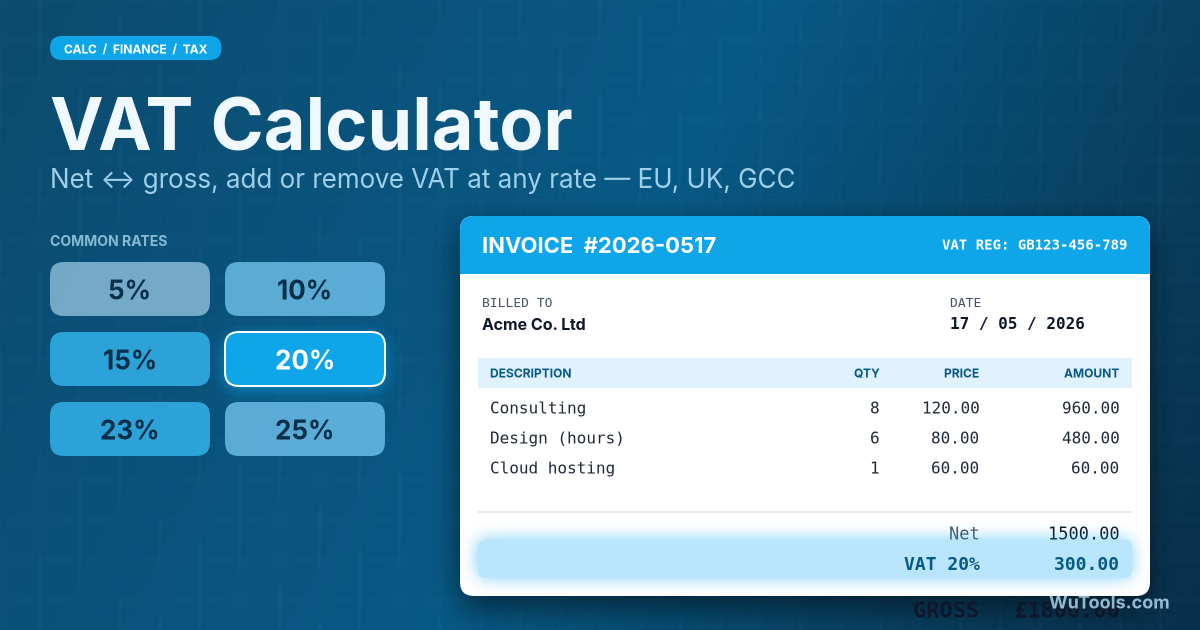

VAT Calculator

For Consumers

Retail prices include VAT in the UK and EU — the price tag is what you pay

Check if business quotes are VAT-inclusive or exclusive — B2B contracts often quote ex-VAT, B2C must be inclusive

Zero-rated items have 0% VAT but the supplier still issues a VAT invoice for traceability

VAT refund schemes exist for non-resident tourists in many countries — claim at the airport on departure

Cross-border online purchases above small-value thresholds carry VAT at the import point — the EU removed the €22 low-value exemption in July 2021

Some services are VAT-exempt: insurance, finance, healthcare, education in most VAT regimes

VAT Registration Thresholds (2026)

Each country sets its own threshold for compulsory VAT registration. Below the threshold, registration is voluntary; above it, mandatory.

United Kingdom: £90,000 in any 12-month rolling period (raised from £85,000 on 1 April 2024)

Germany: €25,000 for the small-business scheme (raised from €22,000 on 1 Jan 2025)

Ireland: €40,000 for services, €80,000 for goods

France: €37,500 for services, €91,900 for goods (auto-entrepreneur thresholds)

Netherlands: €20,000 for the small-business scheme (KOR)

EU cross-border B2C sales: €10,000 EU-wide threshold; over this you need to register or use OSS

Voluntary registration is always allowed and often profitable for input-reclaim purposes

When to Use This Calculator

Pricing products: convert a net target into a customer-facing gross price

Invoicing: cross-check VAT breakdown against your accounting software

Expense reports: extract the VAT element from receipts for input reclaim

Preparing VAT returns: reconcile gross and net totals

Cross-border purchases: estimate the landed cost including import VAT

Verifying supplier invoices match the stated rate

Comparing supplier quotes when one is ex-VAT and another inc-VAT

Quick sanity check of automated VAT calculations in e-commerce checkouts

VAT vs Sales Tax (and the Asia/Commonwealth GST/SST family)

All three tax families have one job — tax final consumption — but operate very differently:

VAT (most of the world): multi-stage, value added at each step, businesses reclaim input VAT

Sales tax (US states): single-stage, applied only at final retail sale, no business reclaim

GST (Australia, NZ, Canada, Singapore, India): functionally identical to VAT, different name

Malaysia SST and Pakistan FED: split-rate hybrids closer to single-stage sales tax than to VAT

VAT paper trail makes tax evasion harder; sales tax is simpler but less self-enforcing

The big design choice: input-VAT credit chain (VAT/GST) vs single-point collection (sales tax)

Frequently Asked Questions

Every time you click Add VAT or Remove VAT, the result is appended as a new row, and a Totals footer below the table sums the Net, VAT and Gross columns live. This turns the calculator into a multi-line reconciliation pad: enter each invoice line (or each receipt in an expense batch) one at a time, switching the rate or country between rows as needed — say 20% on one item and 5% on another — and the footer keeps a running tally of all three columns. It is exactly the task a bookkeeper does when preparing a quarterly VAT return: the Net total is your box for total sales/purchases excluding VAT, the VAT total is the tax to declare, and the Gross total is the cash figure that should match your bank or ledger. Because rows accumulate, you can mix Add-VAT lines (net entered) and Remove-VAT lines (gross entered) in the same batch and still get correct grand totals. Press Clear results to empty the table and reset the footer to zero before starting a new batch.

VAT is the European primary source of indirect revenue, often 20-25% — high enough to fund universal healthcare, education and social spending. US states use sales taxes of typically 5-10% (some go higher with combined state + local, but rarely above 11%), with the federal government relying on income taxes instead. The political economy is path-dependent: Europe introduced VAT through the 1960s-70s as a unified harmonized system across what became the EU, with mandatory minimums (currently 15% standard, 5% reduced floor under EU rules); the US has 50 separate state tax bases that resist harmonization. The deeper structural difference is incidence: VAT is regressive on its own (poor families spend a higher fraction of income), but European countries pair high VAT with strong progressive income tax and direct transfers, netting out to a flatter overall tax system. US sales tax + flat-ish federal income tax + low transfers produces more inequality, not less.

The UK VAT rate didn't change post-Brexit — it's been 20% standard since 4 January 2011. What changed dramatically is cross-border treatment with the EU. Pre-2021, UK businesses selling to EU consumers used the Distance Selling thresholds (€35,000 or €100,000 depending on country); post-2021, every UK-to-EU B2C sale generates an import VAT obligation in the destination country, payable either by the buyer at import or by the seller via IOSS (Import One-Stop Shop). UK-to-EU B2B uses zero-rating with proof of export. UK companies importing from the EU now pay UK import VAT plus customs duty. The £90,000 UK registration threshold (raised from £85,000 in April 2024) is one of the highest in Europe; many small businesses operate below it deliberately to avoid VAT admin. Northern Ireland is the strange exception: it remains in the EU VAT system for goods but not services under the Windsor Framework, giving NI businesses dual access.

Finland's standard VAT was raised from 24% to 25.5% on 1 September 2024 — the highest standard rate in the EU, edging out Sweden, Denmark, Norway and Croatia (all 25%) and trailing only Hungary's 27% globally. The reason was fiscal: Finland's deficit and debt-to-GDP had drifted above EU targets, and a centre-right coalition in Helsinki chose VAT increases over income-tax rises to repair the public finances. The political logic is that VAT increases are politically easier than visible income-tax hikes (consumers feel each purchase less than each paycheck). The unusual 25.5% half-point illustrates the precision EU finance ministries now use to fine-tune revenue. For businesses operating in Finland, the rate change required reconfiguring POS, ERP and accounting systems within a tight window, with a transition period for invoices spanning the rate change. The reduced rates (14% and 10%) are mostly unchanged, though books moved from 10% to 14% in 2023.

Output VAT is what you charge customers on your sales. Input VAT is what you pay suppliers on your business purchases. The VAT you actually remit to the tax authority is output minus input — that's the 'value added' you contributed in the supply chain. Example: you sell €1,000 of consulting at 20% VAT, charging the customer €1,200 (output VAT = €200). You bought €300 of software subscriptions with 20% VAT, paying the supplier €360 (input VAT = €60). Net VAT to remit = €200 − €60 = €140. If input exceeds output (common in your first year, exports, or capital-investment phases), you get a refund from the tax authority. Two traps: (1) you can only reclaim input VAT if the purchase relates to taxable supplies — buying a car for personal use, no reclaim; (2) some inputs are restricted by jurisdiction (UK doesn't allow most entertainment VAT reclaim, business meal VAT is capped in many countries).

Divide the gross by (1 + VAT rate as decimal). A £120 inclusive price at 20% gives net = 120 / 1.20 = £100, VAT = £20. The common mistake is to compute 'VAT = 120 × 20% = £24', subtract for £96, add 20% to verify, and discover £115.20 — not £120. The asymmetry exists because VAT is a percentage of the NET (smaller) base, not the gross. Quick mental shortcuts: for 20% VAT, divide gross by 6 to get VAT (£120 / 6 = £20); for 19% German VAT, divide by 6.26; for 25% Nordic VAT, divide by 5. For Finland's 25.5%, the multiplier is 25.5/125.5 = 0.2032 — gross × 0.2032 = VAT. Memorizing the multiplier for your most-used rate saves a lot of time in monthly reconciliations.

For EU consumers, the destination-country rate applies — a UK SaaS company selling to a German consumer charges 19% German VAT, not 20% UK VAT, even though the seller is in the UK. The compliance burden used to mean registering in every EU country, but the OSS (One-Stop Shop) and non-EU IOSS regimes let you declare and pay all EU VAT through a single quarterly return in your home country (or your chosen EU country if you're outside the EU). The rules for B2B are different — reverse charge applies, so the seller charges 0% and the buyer self-accounts for VAT in their country. The threshold for triggering destination-country rules in the EU is €10,000 of cross-border B2C sales per year; below this, you can keep charging your home rate. The US and most non-EU jurisdictions have similar 'remote seller' rules: South Dakota v Wayfair (2018) created economic nexus thresholds (typically $100,000 or 200 transactions) requiring registration in any US state where you sell.

In many countries, yes — through 'tax-free shopping' or VAT refund schemes for non-resident travelers. The classic example: a non-EU visitor buying a €1,000 watch in Paris at 20% VAT can reclaim the €200 by getting a tax-free form from the retailer, having it stamped at the airport customs counter on departure, and either receiving cash at a refund desk (with a 15-30% commission) or a credit-card refund weeks later. Minimum purchase thresholds vary: France €100.01, Germany €25, Italy €70.01, Spain €0 (no minimum since 2018), UK was £30 until the scheme was abolished post-Brexit in 2021. The UAE has a tourist VAT refund for purchases over AED 250. Tourist VAT refund schemes are politically popular because they pull luxury spending from cross-border shoppers, but they're administratively expensive — many shops charge the commission so high that the cash refund is effectively a marketing tool, not a real tax break.

Reverse charge shifts the VAT-accounting responsibility from the seller to the buyer. Instead of the seller charging VAT and remitting it, the buyer self-accounts for the VAT — recording both output and input VAT on the same return, with net effect zero (assuming the input is reclaimable). It's used in three common scenarios. (1) EU cross-border B2B services: a Dutch consultancy invoicing a German business charges 0%, the German business self-accounts for 19% German VAT and reclaims it the same return. (2) Domestic anti-fraud reverse charge: UK construction services (CIS reverse charge since March 2021) and trades in mobile phones/CPUs to prevent missing-trader fraud. (3) Imports from outside the EU under the postponed VAT accounting regime. The benefit: less cash tied up in VAT, less paperwork for cross-border invoices. The risk: if the buyer isn't VAT-registered or forgets to self-account, the tax can go uncollected — which is why all three scenarios require strict B2B/CIS-registration verification.