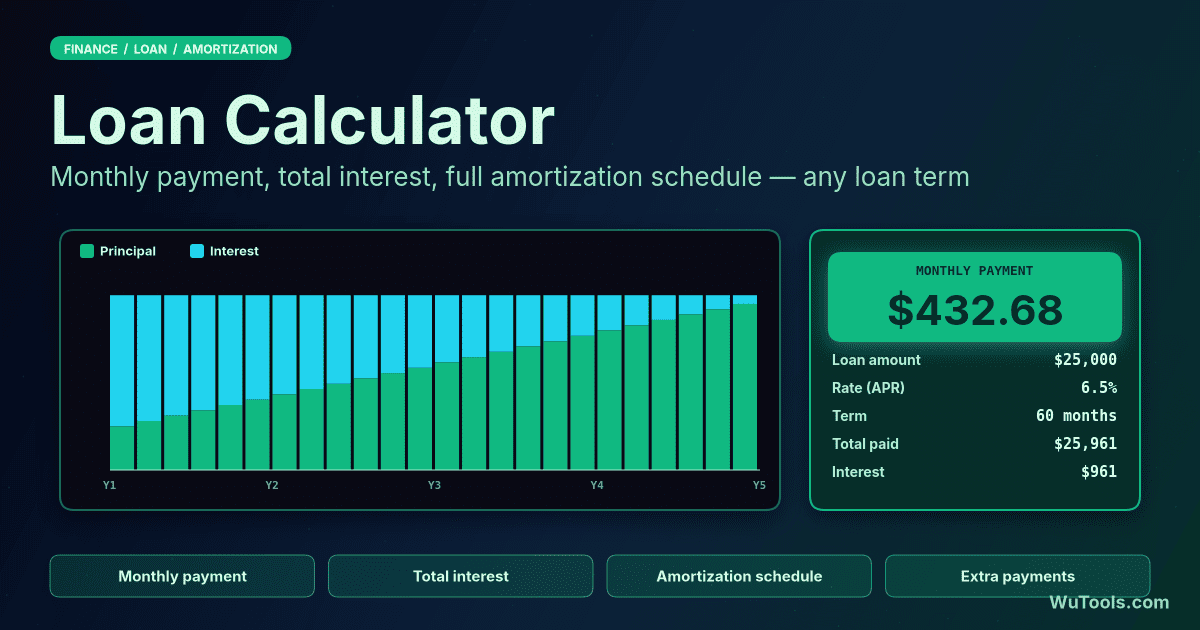

Loan Calculator

Calculate loan payments, total interest and a full amortization schedule with extra payments and APR/APY. Export the dated schedule to CSV.

Amortized Loan: Paying Back a Fixed Amount Periodically

Use this calculator for basic calculations of common loan types such as mortgages, auto loans, student loans, or personal loans, or click the links for more detail on each.

Deferred Payment Loan: Paying Back a Lump Sum Due at Maturity

Use this calculator to determine the future value of a loan where no payments are made until maturity. Interest compounds over the loan term.

Bond: Paying Back a Predetermined Amount Due at Loan Maturity

Use this calculator to compute the initial value of a bond/loan based on a predetermined face value to be paid back at bond/loan maturity.

What is a Loan Calculator?

A loan calculator is a versatile financial tool designed to help you understand the true cost of borrowing money. Whether you're considering a mortgage, auto loan, student loan, or personal loan, this calculator provides detailed insights into your payment obligations, total interest costs, and repayment schedules.

This comprehensive loan calculator includes three different calculation methods to cover various loan types: Amortized Loans (regular periodic payments), Deferred Payment Loans (lump sum at maturity), and Bonds (present value calculations). Each type serves different financial needs and understanding them helps you make informed borrowing decisions.

Amortized Loan: Fixed Periodic Payments

An amortized loan is the most common type of loan where you make regular, equal payments over the loan term. Each payment includes both principal and interest, with the proportion shifting over time. Early payments are mostly interest, while later payments are mostly principal.

The formula for calculating the periodic payment amount is:

PMT = P × [r(1+r)n] / [(1+r)n - 1]

Where:

- PMT = Payment amount per period

- P = Principal loan amount (initial amount borrowed)

- r = Interest rate per payment period

- n = Total number of payments

Deferred Payment Loan: Lump Sum at Maturity

A deferred payment loan is a type of loan where no payments are made during the loan term. Instead, interest accrues and compounds, and the entire amount (principal plus accumulated interest) is paid at maturity. This is common in certain investment vehicles, student loans during school years, or specialized financial products.

The formula for calculating the amount due at maturity is:

A = P(1 + r/n)nt

Where:

- A = Amount due at maturity (future value)

- P = Principal loan amount (initial amount borrowed)

- r = Annual interest rate (as decimal)

- n = Number of times interest compounds per year

- t = Time in years

Bond: Present Value of Future Amount

A bond calculation determines how much you would receive today (present value) for a loan that requires you to pay back a specific amount in the future. This is essentially the reverse of the deferred payment loan - instead of knowing what you borrow and calculating what you'll owe, you know what you'll owe and calculate what you can borrow today.

The formula for calculating the present value (amount received at start) is:

P = F / (1 + r/n)nt

Where:

- P = Present value (amount received when loan starts)

- F = Future value (predetermined amount due at maturity)

- r = Annual interest rate (as decimal)

- n = Number of times interest compounds per year

- t = Time in years

Practical Examples

Example: Amortized Loan

A $100,000 loan at 6% annual interest for 10 years with monthly payments:

- Loan Amount: $100,000

- Interest Rate: 6% per year (compounded monthly)

- Loan Term: 10 years (120 months)

- Payment Frequency: Monthly

- Monthly Payment: $1,110.21

- Total Payments: $133,224.60

- Total Interest: $33,224.60

- Principal: 75% | Interest: 25%

Example: Deferred Payment Loan

A $100,000 loan at 6% annual interest for 10 years with no payments (compounded annually):

- Loan Amount: $100,000

- Interest Rate: 6% per year (compounded annually)

- Loan Term: 10 years

- Payment Frequency: None (deferred)

- Amount Due at Maturity: $179,084.77

- Total Interest: $79,084.77

- Principal: 56% | Interest: 44%

Example: Bond Calculation

A bond requiring $100,000 payment in 10 years at 6% annual interest (compounded annually):

- Amount Due at Maturity: $100,000

- Interest Rate: 6% per year (compounded annually)

- Loan Term: 10 years

- Amount Received Today: $55,839.48

- Total Interest Paid: $44,160.52

- Principal: 56% | Interest: 44%

Common Loan Types and Applications

- Mortgages: Home loans typically use amortized payment structures with 15-30 year terms. Fixed-rate mortgages have constant payments, while adjustable-rate mortgages (ARMs) can change.

- Auto Loans: Vehicle financing usually follows amortized schedules with 3-7 year terms. New cars often qualify for better rates than used vehicles.

- Student Loans: Education loans may be deferred during school (interest accrues) then switch to amortized payments after graduation. Federal and private loans have different terms.

- Personal Loans: Unsecured loans for various purposes, typically amortized over 2-7 years. Interest rates vary based on creditworthiness.

- Business Loans: Commercial financing can use any structure - amortized for equipment purchases, deferred for startups, or balloon payments for real estate.

- Bonds and Securities: Corporate and government bonds pay a fixed amount at maturity, with the purchase price reflecting present value calculations.

- Payday and Short-term Loans: High-interest loans with lump sum repayment, often due in 2-4 weeks. Generally expensive and risky.

- Interest-Only Loans: Pay only interest during initial period, then either balloon payment or convert to amortized schedule.

Tips for Managing Loans

- Compare APR vs APY: APR (Annual Percentage Rate) shows simple interest, while APY (Annual Percentage Yield) includes compounding effects. Higher compounding frequency means higher effective rate.

- Extra Payments: Additional principal payments on amortized loans reduce total interest significantly. Even small extra payments early in the loan term make a big difference.

- Shorter Terms Save Money: Loans with shorter terms have higher monthly payments but much lower total interest. A 15-year mortgage costs far less than 30-year, even at similar rates.

- Shop Around for Rates: Interest rates vary significantly between lenders. A difference of 0.5% can mean thousands in savings over the loan term.

- Consider Total Cost: Don't focus only on monthly payment - calculate total interest paid over the life of the loan. Lower payments often mean more interest.

- Understand Compound Frequency: Monthly compounding is more expensive than annual compounding at the same stated rate. Know how your loan compounds.

- Deferred Interest Risks: Loans with deferred payment can balloon to unexpected amounts. Interest compounds on interest, growing the balance exponentially.

- Credit Score Matters: Better credit scores qualify for lower interest rates, saving substantial money. Work on improving credit before applying for major loans.

- Read the Fine Print: Watch for prepayment penalties, variable rates, balloon payments, and other terms that could cost extra or create payment surprises.

- Emergency Fund First: Before taking on new debt, ensure you have 3-6 months of expenses saved. This prevents defaulting if financial situations change.

When to Use Each Loan Type

- Use Amortized Loans When: You want predictable monthly payments, are financing a home or vehicle, need to build equity gradually, or prefer consistent budgeting with no surprises at maturity.

- Use Deferred Payment Loans When: You expect higher future income (like students), need to minimize current cash flow obligations, have investments earning more than loan interest, or are handling short-term cash flow issues.

- Use Bond/Present Value When: You're pricing investment securities, comparing loan offers, determining fair value of future obligations, or structuring business deals with future payments.

- Avoid Deferred Loans When: Interest rates are high (compounding costs explode), you're uncertain about future income, the loan term is very long, or you have trouble managing growing obligations.

- Refinancing Considerations: Refinance amortized loans when rates drop 1%+, you can shorten term without payment stress, you can eliminate PMI, or you need to convert variable to fixed rates.