Calculate monthly mortgage payment with full PITI breakdown, amortization, auto PMI, property tax, insurance, HOA, and refinance break-even. Free and fast.

Have feedback? Report bugs, suggest features, or share your thoughts — we read them all

What is a Mortgage Calculator?

A mortgage calculator turns three numbers — loan amount, annual interest rate, and term — into the monthly payment that pays the loan off exactly at the end. Behind the simple output is the standard amortization formula, which front-loads interest in the early years and shifts to principal in the later years. The same $300,000 loan at 6% for 30 years costs $1,798.65/month; over the life of the loan you pay $647,514.57 total, of which $347,514.57 is interest — more than the original loan.

Modern mortgage calculators do more than the payment. They show you the amortization schedule (how every payment splits into principal vs interest), the impact of extra payments, when PMI drops off (at 78% loan-to-value automatically, 80% on request), and whether refinancing actually saves you money after closing costs. Use it before house-hunting to set a budget, when comparing 15-year vs 30-year terms, when shopping rates, and again every year to see if refinancing is worth it.

Mortgage Payment Formula

The standard amortization formula for a fixed-rate mortgage:

M = P × [R(1+R)N] / [(1+R)N - 1]

Where:

M = Monthly Payment (principal + interest only, before taxes/insurance)

P = Principal Loan Amount (the amount you borrow)

R = Monthly Interest Rate (Annual Rate / 12 — so 6% APR = 0.5% monthly)

N = Total Number of Monthly Payments (Years × 12, so 30-year = 360)

Example Calculation

For a $300,000 mortgage at 6% annual interest for 30 years:

Total Interest Paid: $347,514.57 — 116% of the original loan

Types of Mortgages

Fixed-Rate Mortgage: Interest rate stays the same for the entire term — 30-year is the US default, 15-year saves enormous interest at a higher monthly cost

Adjustable-Rate Mortgage (ARM): Fixed initial period (5, 7, 10 years), then rate adjusts annually — risky if rates rise, common labels are 5/1, 7/1, 10/1

FHA Loan: Government-backed, down payment as low as 3.5%, easier credit requirements but PMI for the life of the loan if you put down less than 10%

VA Loan: Available to qualified veterans with zero down payment and no PMI — one of the best loan products in the US market

USDA Loan: Zero-down for rural and some suburban areas, income-limited, US-only

Conventional Loan: Not government-insured, usually 5-20% down, PMI required under 20% equity

Jumbo Loan: For amounts exceeding conforming limits (currently $766,550 in most US counties, higher in expensive areas)

Interest-Only Mortgage: Pay only interest for an initial period (5-10 years), then full amortization kicks in — payment shock is severe

Reverse Mortgage: For seniors 62+, converts home equity to cash with no monthly payments — repaid when you sell or pass away

Factors Affecting Mortgage Payments

Principal Amount: Every $10,000 less borrowed saves about $60/month at 6% over 30 years

Interest Rate: A 1% rate change moves a $300,000 30-year payment by about $185/month — rates are by far the biggest lever

Loan Term: 30-year payment is ~$1,799, 15-year is ~$2,531 — the 15-year saves ~$192,000 in total interest

Down Payment: Larger down payment reduces both the principal and the need for PMI

Property Taxes: 1.1% of home value on average in the US, paid via escrow with the lender

Homeowners Insurance: $1,400-$2,000/year typical, also escrowed

PMI (Private Mortgage Insurance): 0.5-1.5% of the loan annually, required when LTV exceeds 80%, drops off automatically at 78% LTV

HOA Fees: $200-$700/month typical in condos and managed communities, not included in mortgage but eats budget

Mortgage Calculator

Mortgage Planning Tips

Shop 3-5 lenders within a 14-day window — credit bureaus treat it as one inquiry, and rate quotes vary by 0.25-0.5%

Compare APR, not just interest rate — APR includes lender fees and is the apples-to-apples number

Pay attention to discount points: 1 point = 1% of the loan, lowers the rate, only worth it if you'll stay long enough to break even

A 20% down payment avoids PMI but a 10% down payment with PMI is often the right move if you'd otherwise wait years to save

Get pre-approved (not just pre-qualified) before house hunting — sellers don't take pre-qualified offers seriously

Make one extra payment per year on a 30-year mortgage and you'll pay it off in about 25 years, saving tens of thousands in interest

Don't drain emergency savings for a larger down payment — keep 3-6 months of expenses liquid

Re-shop insurance and taxes every 2-3 years — your escrow can quietly grow by $200/month if you don't

How Much Mortgage Can You Afford?

The classic 28/36 rule from the FHA still holds in 2026:

Front-end ratio: Housing costs (PITI — principal, interest, taxes, insurance) should not exceed 28% of gross monthly income

Back-end ratio: All debt payments (mortgage + car + student loans + credit cards) should not exceed 36% of gross income

Emergency fund: 3-6 months of full PITI plus living expenses, in cash or treasuries

Closing costs: Budget 2-5% of home price separately — they are NOT rolled into the loan in most US mortgages

Future expenses: Children, healthcare, college, retirement — don't sacrifice all of them for housing

Maintenance: Budget 1-2% of home value per year for repairs, paint, HVAC, roof — it averages out even if you don't spend it yearly

When to Consider Refinancing

Rates have dropped at least 0.75-1.0% below your current rate (old 1-2% rule is outdated with lower-cost lenders)

Your credit score has jumped 50+ points since closing — your old rate may be priced for old you

You want to switch from an ARM to a fixed rate before the adjustment period ends

You want a shorter term — refinancing a 30-year into a 15-year at a lower rate can save six figures

You have 20%+ equity and want to drop PMI — sometimes a refinance is faster than waiting for amortization

You want a cash-out refinance for home improvements (which add value) — not for vacations or cars

Break-even rule: closing costs / monthly savings = months to recoup. If you'll move before then, refinancing loses money

Frequently Asked Questions

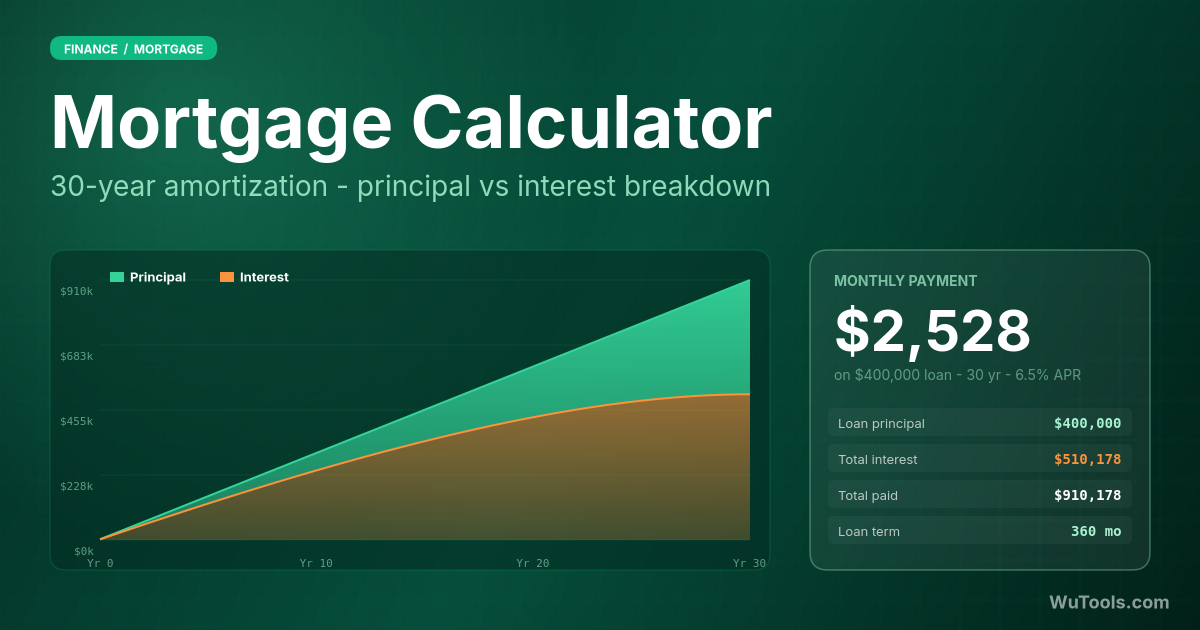

Because the formula charges interest on the outstanding balance, and in month 1 the balance is the entire loan amount. For a $300,000 / 6% / 30-year mortgage, month 1's interest is $300,000 × 0.005 = $1,500, leaving only $298.65 for principal out of the $1,798.65 payment. The balance drops slowly at first — after 5 years you've paid $107,919 total but only $20,635 of principal, while $87,284 went to interest. The crossover where each monthly payment is half principal and half interest doesn't arrive until around year 18 of a 30-year mortgage. This is why making extra principal payments early is so powerful: every $1 of extra principal in year 1 saves $5.74 of interest over the life of a 6% / 30-year loan, because it removes 30 years of compounding from that dollar. Late extra payments matter much less.

Mathematically, almost always yes — but it depends on your other priorities. A $300,000 loan at 6%: 30-year = $1,798.65/mo, total interest $347,514; 15-year (typically 0.5% lower rate, so ~5.5%) = $2,451/mo, total interest $141,153. You save about $206,000 in interest with the 15-year. But you pay $652 more per month, which is $652 you can't invest, can't keep liquid, and can't use for emergencies. The optimal strategy for many people is: take the 30-year for safety, but pay it like a 15-year voluntarily — same interest savings, full flexibility to drop back to the lower payment in a bad month. The only reason to legally commit to the 15-year is the lower interest rate, and that gap shrunk from 0.75% to 0.25% in recent years, weakening the case for the 15-year contract.

Interest rate is what you pay on the loan; APR (Annual Percentage Rate) is the interest rate plus mortgage-related fees expressed as an annualized cost. Required by the Truth in Lending Act, APR includes origination fees, discount points, mortgage insurance premiums in some cases, and lender fees, but not third-party costs like appraisal or title insurance. A 6.0% loan with $5,000 in origination fees on a $300,000 loan has an APR around 6.18%. APR is the right number for comparing offers across lenders because it normalizes the fee structure — a 5.95% loan with $8,000 in fees can actually cost more than a 6.05% loan with $0 in fees, and the APR will show it. The trap: APR assumes you hold the loan the full term. If you refinance or move in year 5, the upfront fees hurt much more proportionally, and the headline APR understates the real cost.

Calculate the break-even point: closing costs divided by monthly savings. Example: rates dropped from 7.5% to 6.0%, your $300,000 / 30-year payment falls from $2,098 to $1,799, saving $299/month. Refinancing closing costs are about $6,000 (2% of loan). Break-even = $6,000 / $299 = 20 months. If you plan to stay in the house longer than 20 months, refinancing wins; if you'll sell within 18 months, you lose money. Also account for the reset of the amortization clock — refinancing your 7-year-old 30-year loan into a new 30-year resets the calendar and front-loads interest again, so total lifetime interest can actually go up even though monthly payment drops. The fix: refinance into a 20-year or 15-year if you can afford it, or apply your monthly savings as extra principal on the new loan to keep the original payoff date.

Yes — disproportionately so, because each extra principal dollar removes its own future interest charges from the schedule. On a $300,000 / 6% / 30-year mortgage, paying an extra $200/month from day one shortens the term by 5.6 years and saves $87,200 in interest. One extra payment per year (twelve $150 add-ons or one $1,800 lump in December) saves about $54,000 and shaves 4.5 years off. The earlier the extra payment, the bigger the impact: $10,000 in year 1 saves about $36,000 of interest, but the same $10,000 in year 20 saves only $4,200. Two cautions: make sure your lender applies extra payments to principal (write 'PRINCIPAL ONLY' on the check or use the principal-payment option in the app), and don't sink emergency reserves into the mortgage — liquid cash earning 4% in a money market is still better than illiquid equity, in any economy where you might lose your job.

Private Mortgage Insurance protects the lender (not you) if you default with less than 20% equity. It's required on most conventional loans with under 20% down, and costs 0.5-1.5% of the loan annually — on a $300,000 loan that's $125-$375/month, with no benefit to you. There are three ways out. (1) Automatic termination: by federal law (Homeowners Protection Act), PMI must drop off automatically when your scheduled loan-to-value hits 78%, based on the original amortization schedule. For a 90%-LTV loan at the start, that's around year 11. (2) Requested cancellation at 80% LTV: you can ask the lender to remove PMI as soon as your scheduled balance hits 80% of original value, which is faster than the automatic 78% — usually a small saving but worth one phone call. (3) Reappraisal: if your home has appreciated and you're now at 80%+ equity based on current value, a $500 appraisal can remove PMI years early — often the highest-ROI house decision after refinancing. FHA loans are different: PMI ('MIP') is permanent unless you originally put 10%+ down, in which case it drops at year 11. To escape FHA MIP you usually have to refinance into a conventional loan.

Three big effects beyond the obvious lower loan amount. (1) Interest rate tier: most lenders offer slightly better rates at 20%+ down (0.125-0.25% lower), because LTV under 80% is less risky for them. (2) PMI: under 20% down triggers monthly PMI of 0.5-1.5% of the loan, often $150-$400/month on a typical loan. (3) Closing-cost ratio: many fees are flat dollars, so a smaller loan amortizes those costs over fewer dollars — APR rises slightly. The math: a $400,000 home with 5% down vs 20% down at the same 6% rate. 5%-down loan ($380,000): $2,278/mo P+I + ~$300 PMI = $2,578. 20%-down loan ($320,000): $1,918/mo P+I, no PMI. The 20% scenario saves $660/month but requires $60,000 more cash up-front. Break-even: $60,000 / $660 = 91 months = 7.5 years. If you'd otherwise have invested that $60,000 at 7% return, the 5%-down case wins by year 15 — so the choice depends on your investment alternatives, not just on housing math.

Most US mortgages bundle property taxes and homeowner's insurance into the monthly payment, paid into an escrow account that the lender holds and pays out twice a year (taxes) and annually (insurance). Your monthly payment is therefore PITI: Principal + Interest + Taxes + Insurance. Principal and interest are fixed for a fixed-rate loan, but taxes and insurance change. Property tax assessments rise as your local government reappraises (often automatic with home values), and homeowners insurance has risen 30-40% nationally since 2020 due to hurricane/wildfire claims and reinsurance costs. Your escrow analysis once a year recalculates the required monthly contribution; if the prior year's escrow ran short, the lender catches it up over the next 12 months and your payment can jump $100-$300/month. To avoid surprises: appeal your property tax assessment annually (50%+ of appeals succeed), shop insurance every 2-3 years, and pad your own savings rather than trusting the lender's escrow buffer.

Lenders qualify you on your full PITI payment (principal + interest + taxes + insurance + PMI + HOA), not on bare principal and interest — which is exactly why this calculator now shows the PITI total. The classic 28/36 rule: your housing PITI should stay under 28% of gross monthly income (front-end ratio), and ALL debt payments — PITI plus car loans, student loans, and minimum credit card payments — should stay under 36% (back-end ratio). Worked example: a household earning $9,000/month gross can carry up to $2,520 in PITI (28%) and $3,240 in total debt (36%). If they already pay $600/month in car and student loans, the back-end test caps PITI at $3,240 − $600 = $2,640, but the front-end test is stricter at $2,520, so $2,520 is the real ceiling. Notice this is PITI, not P&I: at a 6% rate, $2,520 PITI on a 30-year loan only supports about $1,950 of principal and interest once you reserve roughly $370/month for taxes, $125 for insurance, and any PMI — which is the difference between a $325,000 loan and a $370,000 loan. Many lenders stretch to 43% or even 50% back-end for strong credit, but borrowing to the 28/36 limits keeps you safer against rate resets, escrow increases, and job loss.