Add or remove GST from inclusive or exclusive prices: Australia 10%, Canada 5%, India, NZ 15%, Singapore 9%. Totals reconcile to the cent for BAS and invoices.

Have feedback? Report bugs, suggest features, or share your thoughts — we read them all

What is GST?

GST (Goods and Services Tax) is a value-added consumption tax levied on most goods and services. Businesses collect it on behalf of the government — they charge GST on sales (output tax) and reclaim GST on business purchases (input tax credit), remitting only the difference. The final consumer ultimately pays it. Around 170 countries use some form of GST/VAT, with rates from 5% (Canadian federal GST) up to 27% (Hungary VAT).

Two operations matter: ADDING GST when you're a seller quoting a net price and need the gross price the customer pays, and REMOVING GST when you have an inclusive invoice and need to know the tax component (for input tax credit claims or expense reports). This calculator does both with one click, using the current rates for Australia (10%), Canada (5% federal), India (4 slabs from 5% to 28%), New Zealand (15%), Singapore (9% since January 2024) and others.

GST Calculation Formulas

Two operations, two formulas — the second is the inverse of the first:

Australia: 10% (single rate, applied to most goods and services)

Canada: 5% federal GST + provincial PST/HST/QST (combined ~5% to 15%)

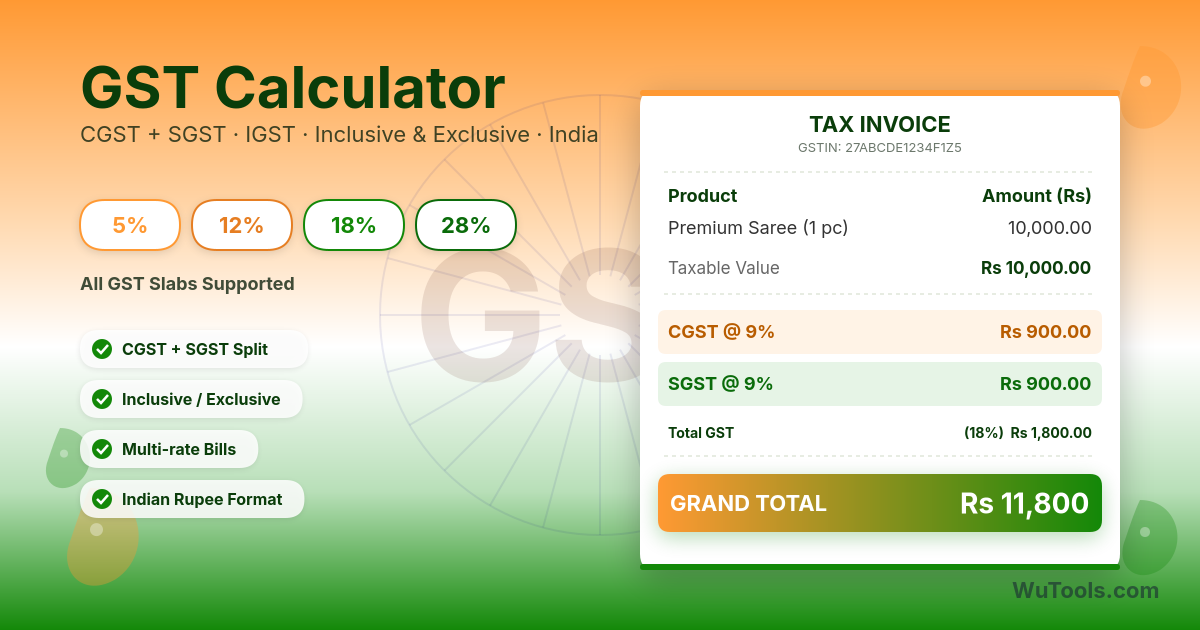

India: 5%, 12%, 18%, 28% (four slabs, plus 0% for essentials)

Malaysia: GST was 6% but replaced by SST (Sales and Service Tax) in 2018

New Zealand: 15% (single rate, broad-based)

Singapore: 9% (raised from 8% on 1 January 2024)

Hong Kong: No GST or VAT system

European Union: 17% (Luxembourg) to 27% (Hungary), with reduced rates for essentials

For Business Owners

Register for GST when you exceed the threshold — A$75,000 in Australia, S$1M in Singapore, ₹40 lakh in India

Voluntary registration can be worth it below threshold if most of your input costs include reclaimable GST

Issue tax-compliant invoices: include your registration number, GST amount as separate line, and gross total

Reconcile input tax credits monthly — unclaimed credits become permanent leaks of working capital

Track exempt vs zero-rated supplies separately — both have 0% output but only zero-rated allows full input credit

Submit returns on time: late lodgement carries flat penalties plus daily interest in most countries

Keep GST records 5-7 years (varies by jurisdiction) — audits commonly look back this far

Use accounting software with GST reporting built-in (Xero, MYOB, QuickBooks, Tally for India)

GST Calculator

For Consumers

Check whether quoted prices include or exclude GST — in Australia, NZ and Singapore retail prices must be inclusive; in many US-style B2B quotes they're exclusive

Business travelers can often reclaim GST on overseas purchases through tourist refund schemes — keep receipts

Some items are GST-free in some countries: fresh food and prescription drugs in Australia, dairy/cereal in NZ, exports universally

Online imports often have a GST threshold — Australia removed it for low-value items in 2018, the EU did the same in 2021

Restaurant bills and service charges may have GST applied on top — read the bill carefully

Compare gross prices when shopping cross-border to avoid surprise tax at customs

Common GST-Free or Zero-Rated Items

Most GST regimes exempt or zero-rate categories the government deems essential. The list varies but commonly includes:

Basic foods (fresh produce, bread, milk in many countries)

Healthcare, prescription medicines, and most medical services

Education (school and tertiary tuition)

Financial services (loans, insurance, currency exchange — often exempt rather than zero-rated)

Residential rent (landlords cannot charge GST on long-term residential rent)

Charitable activities by registered nonprofits

Exports (zero-rated — supplier reclaims input GST, customer pays nothing)

International transport and tourism services in some countries

When to Use This Calculator

Pricing products: turn a target net price into a customer-facing gross price

Issuing invoices: confirm the GST breakdown matches your invoicing software

Reconciling expense reports: extract the GST component from inclusive receipts

Preparing BAS / GST returns: cross-check the inclusive vs exclusive totals

Budgeting cross-border purchases: estimate the final landed cost

Verifying supplier invoices match the stated rate

Quickly evaluating quotes that mix GST-inclusive and GST-exclusive presentations

Comparing prices fairly across countries with different GST rates

Frequently Asked Questions

Mechanically, yes — both are multi-stage consumption taxes on the value added at each step of production, collected by businesses and ultimately paid by the final consumer. The name differs by tradition: ex-Commonwealth countries (Australia, Canada, India, New Zealand, Singapore) call it GST; most of Europe, Latin America, and Africa call it VAT. The mechanics are identical: input tax credits, output tax, periodic returns. Differences are details — number of rate tiers (Singapore has one, India has four), registration thresholds, what's exempt vs zero-rated. The US is the conspicuous outlier with state-level sales taxes that are single-stage (collected only on the final retail sale), not value-added, which is why US businesses don't reclaim 'input sales tax' the way GST/VAT businesses reclaim input credits.

GST-free and zero-rated mean the same thing in most jurisdictions (Australia uses 'GST-free', NZ uses 'zero-rated'): the seller charges 0% GST on the supply BUT can still reclaim GST paid on related inputs. Exempt is different and worse for the supplier: 0% charged AND no input credit allowed. Example: a registered Australian doctor providing exempt medical services pays GST on their stethoscope and surgery rent but cannot reclaim it — it becomes a cost. A fresh-food exporter, by contrast, charges 0% on exports (zero-rated/GST-free) but reclaims 100% of GST paid on packaging, transport, refrigeration — much better. The trap: governments call things 'GST-free' when they mean zero-rated, but lump exempt items into the same conversational category, so suppliers must check the legislation, not the colloquial term.

9% as of 1 January 2024. The full progression: 3% (1994) → 5% (2003) → 7% (2007) → 8% (2023) → 9% (2024). The two most recent steps came barely 12 months apart — 7% to 8% on 1 January 2023, then 8% to 9% on 1 January 2024 — so companies had to update invoice templates, POS systems and accounting software twice within a year. This calculator uses 9% as Singapore's current rate. The lesson for businesses: GST rate changes are political decisions made with months of notice but always shorter than you'd like; subscribe to your country's tax authority newsletter (IRAS in Singapore, ATO in Australia, CBIC in India) so you're never the last to know. For Canada, the federal GST has been 5% since 2008, but the combined federal-provincial rate (HST) varies — Ontario 13%, Nova Scotia 15%, Quebec 14.975% (QST is technically separate).

Divide the gross price by (1 + GST rate as a decimal), don't subtract. A $110 inclusive price at 10% GST gives net = 110 / 1.10 = $100, GST = $10. A common mistake is to compute 'GST = 110 × 10% = $11', subtract it to get $99, then add 10% to $99 to check — and discover $108.90, not $110. The asymmetry exists because GST is a percentage of the NET (smaller) figure, not the gross. The general formula for any inclusive amount: net = gross × 100 / (100 + rate). For Singapore's 9%: net = gross / 1.09 = gross × 0.9174 (multiplier worth memorizing). For Australia's 10%: net = gross / 1.10 = gross × 0.9091 — the famous 'divide by 11 to get the GST component' shortcut: 110 / 11 = 10, which is exactly the GST.

Federalism. The Canadian constitution gives the federal government and the provinces independent taxation powers. The federal government runs the 5% GST nationally. Provinces independently chose three paths: (1) keep a separate Provincial Sales Tax (PST) — British Columbia, Manitoba, Saskatchewan; (2) replace PST with the Harmonized Sales Tax (HST), which is GST + a provincial portion administered together by Ottawa — Ontario (13%), Nova Scotia, New Brunswick, PEI, Newfoundland (all 15%); (3) keep a parallel system that mirrors GST — Quebec's QST (9.975%, technically not GST but mechanically identical). Alberta, Yukon, NWT, and Nunavut have NO provincial sales tax, only the 5% GST. Practical implication: a SaaS subscription from Toronto to a Toronto customer bills 13% HST as one line; the same subscription from Toronto to a Calgary customer bills 5% GST only. Cross-province B2C is one of the most confusing tax scenarios in the Western world.

Political compromise. When India introduced GST in July 2017 replacing 17 different central and state taxes, the government had to satisfy both luxury-tax-loving states (which wanted high rates on premium goods) and welfare-focused legislators (who wanted essentials taxed minimally). The result: 5% (essentials like packaged food, transport), 12% (computers, fertilizers), 18% (most services and consumer goods — this is the de facto 'standard' rate), 28% (luxury cars, tobacco, premium electronics). Plus 0% for fresh produce, books, services like healthcare. Plus a 'compensation cess' on top of 28% for sin goods. The complexity is famous — and one of the reasons Indian GST compliance software is a $500M+ market. Most regular B2B services land in 18%, which is why this calculator defaults Indian rate to 18% when you select India.

Generally no — input tax credit (ITC) is for business expenses, not personal consumption. An employee's lunch isn't an ITC item; a client lunch usually is (with caveats). Mixed-use items get apportioned: if you use your phone 80% for business and 20% personal, you claim 80% of the GST on the phone bill. Cars are the classic trap: most countries cap the GST-claimable portion of a passenger vehicle at a 'car limit' to prevent businesses from buying personal vehicles through the company. Australia's car limit for 2024-25 is A$69,674, with GST claimable only up to one-eleventh of that. Entertainment expenses are usually NOT claimable (Australian rule), or only 50% claimable (Canada). The defensive move: keep clear separation between business and personal cards, log mixed-use percentages, and ask your accountant before assuming anything is claimable.

Once issued, an invoice creates a tax point — the GST liability arises whether or not you charged it. If you forget the GST line, the customer paid you a GST-inclusive amount whether or not the invoice said so. You owe the tax authority the GST component of the amount received, computed by working backwards (gross / 1.10 for Australia, gross / 1.09 for Singapore, etc.). You can issue an amended invoice or 'tax credit note' to clarify, but you cannot go back to the customer and demand additional GST after the fact unless your contract clearly states prices are exclusive. The lesson: write 'plus GST' or 'GST inclusive' clearly on every quote, contract, and invoice. The cost of clarity is one line of text; the cost of ambiguity is a percentage of every disputed transaction.

Independent rounding. If you round the net, the GST and the gross all separately to two decimals, the three figures can disagree by a cent — e.g. a gross of $109.99 at 9% gives net 100.9083 and GST 9.0817; round each on its own and 100.91 + 9.08 = 109.99 works here, but at other amounts the rounded parts won't sum to the rounded gross, and an auditor will flag the invoice. The fix that ATO and IRAS invoice rules expect is to round only TWO of the three figures and derive the third by subtraction. This calculator now does exactly that: when removing GST it rounds the gross and the net, then computes GST = gross − net; when adding GST it rounds the net and the GST, then computes gross = net + GST. The displayed rows therefore always reconcile to the cent, so you can copy them straight onto a tax invoice or BAS without a balancing adjustment.