Impermanent Loss Calculator

Calculate impermanent loss for Uniswap V2/V3, Balancer weighted & Curve pools. Compare LP vs HODL, add fee-APR break-even, export CSV. Free, in-browser.

What is Impermanent Loss?

Impermanent loss (IL) occurs when you provide liquidity to an automated market maker (AMM) like Uniswap, SushiSwap, or Balancer, and the price of your deposited tokens changes compared to when you deposited them. The greater the price divergence, the more impermanent loss you suffer. It's called "impermanent" because the loss only becomes permanent when you withdraw your liquidity.

What is impermanent loss in DeFi?

Impermanent loss (IL) is the opportunity cost a liquidity provider (LP) experiences when the price ratio of the two assets in an Automated Market Maker (AMM) pool diverges from the ratio at deposit time. Compared to simply holding the two tokens in your wallet, the AMM rebalances by selling whichever token rises (and buying the falling one) to maintain its constant-product invariant (x * y = k for Uniswap V2). When you withdraw, you receive a different ratio of tokens worth less in dollar terms than the unstaked hold position. It's called "impermanent" because if prices return to the original ratio before withdrawal, the loss vanishes — but in practice prices rarely return exactly, so most LP exits realize some loss.

Why is it called "impermanent" if I really lose money?

The name is misleading and many DeFi practitioners prefer "divergence loss" as more accurate. The "impermanent" framing reflects that the loss is unrealized until withdrawal — if prices return to the original ratio, the loss disappears entirely. In practice, prices follow random walks and rarely return exactly, so withdrawing usually crystallizes some divergence loss. The loss is also relative to a benchmark (passive holding), not absolute: in a strong bull market you may still profit in dollar terms but underperform the hold benchmark, while in a crash you may lose less than holding. LP profitability requires trading fees + incentives to exceed this divergence loss plus gas costs over the holding period.

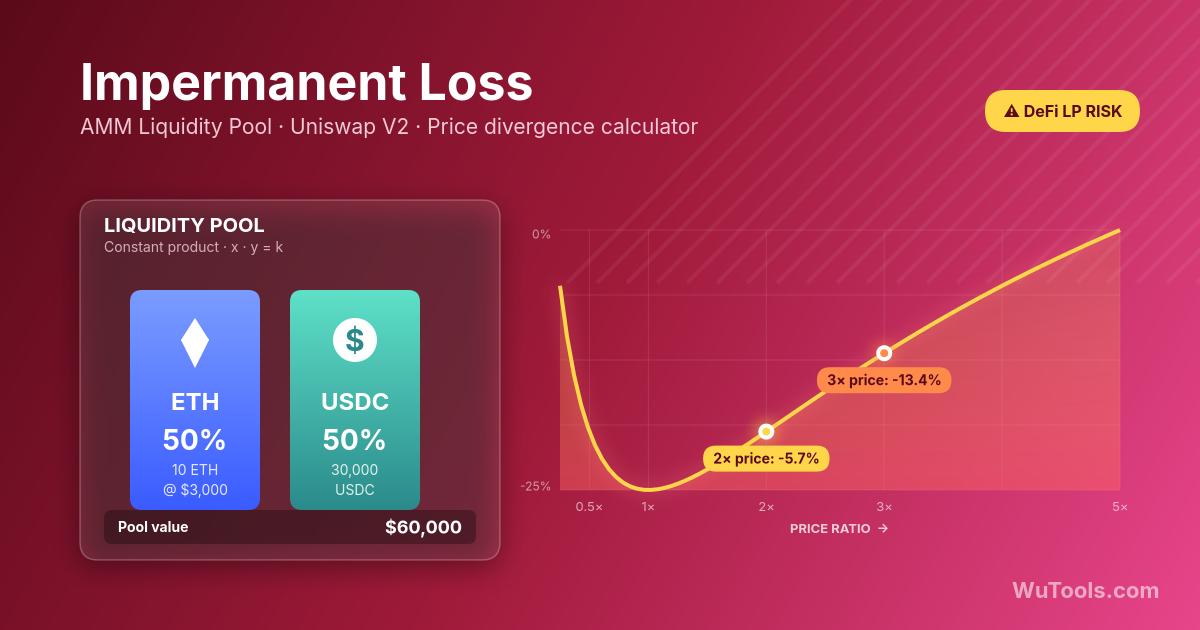

How is impermanent loss calculated for Uniswap V2 pools?

For a constant-product AMM (Uniswap V2, SushiSwap V2 style), the IL formula in terms of the price ratio change is: IL = 2 * sqrt(p) / (1 + p) - 1, where p is the new price ratio divided by the original. A 1.25x price change gives ~0.62% IL; 1.5x gives ~2.02%; 2x gives ~5.72%; 3x gives ~13.4%; 4x gives ~20.0%; 5x gives ~25.5%. Notably the formula is symmetric: a price moving from 1 to 4 has the same IL as moving from 1 to 0.25. The math derives from comparing the AMM's withdrawal value sqrt(k * p_new) to the held value of the original token ratio at p_new. This calculator handles the math automatically — just enter your initial and current prices.

How does Uniswap V3 concentrated liquidity affect IL?

Uniswap V3 (May 2021) introduced concentrated liquidity: LPs choose a specific price range (e.g., ETH between $3000-$4000) and earn fees only when price trades within that range, but with capital efficiency multipliers of 100-4000x versus V2. The catch: IL is amplified by the same multiplier. A 10% price move that causes 0.6% IL in V2 might cause 6-12% IL in a tight V3 range. When price exits the range entirely, your position becomes 100% the depreciating token (single-asset exposure) and earns zero fees until price re-enters. V3 LPing is closer to active options writing than passive yield: profitable for sophisticated LPs who manage ranges with bots (Arrakis, Gamma, Charm); often unprofitable for passive set-and-forget users. Not financial advice.

Can stablecoin pools have impermanent loss?

Yes, but very small. USDC/USDT pools on Curve or Uniswap V3 (with tight $0.99-$1.01 ranges) experience IL only when one stablecoin de-pegs. Historic examples: USDC de-pegged to $0.87 during SVB crisis March 2023 (causing significant IL for USDC/USDT LPs until peg restored), USDT briefly dropped to $0.95 multiple times since 2018, BUSD de-pegged after Paxos halted issuance Feb 2023. A 1% de-peg causes ~0.0025% IL in V2; sustained 5% de-peg causes ~0.063% IL. Curve's specialized StableSwap invariant reduces IL further by using a hybrid constant-sum/constant-product formula in the narrow zone around the peg. The bigger risk for stablecoin LPs is total de-peg (UST May 2022), where one asset collapses to zero. Not financial advice.

When does trading fee income outweigh impermanent loss?

Profitability depends on volume traded relative to liquidity (volume/TVL ratio) and the fee tier. Approximate breakeven: a V2 0.3% pool needs 50-100% annualized volume/TVL for fees to offset moderate IL on volatile pairs. ETH/USDC on Uniswap V2 often had 2-4% APR from fees but 5-15% annualized IL during 2021-2024, making it net-unprofitable for passive LPs. Curve stable pools earn 1-5% APR with near-zero IL, often more reliable. V3 in active ranges can earn 30-100% APR but with proportional IL risk. Always factor in CRV/UNI/SUSHI token incentives, MEV extraction, and gas costs for rebalancing. Many academic studies (Loesch et al. 2021, Tribeca Research 2023) found ~50-70% of Uniswap V2/V3 LPs lose money versus simply holding. Not financial advice.

How do I hedge against impermanent loss?

Sophisticated LPs hedge IL using several techniques: (1) Buy out-of-the-money put and call options on the volatile asset to mimic the AMM's payoff curve (a long-volatility position offsets the short-volatility implicit in LPing); (2) Take a perpetual futures position opposite to the asset accumulation direction — if your ETH/USDC pool tends to accumulate ETH as it falls, short ETH perps; (3) Use IL-protection wrappers like Bancor V3's single-sided staking (paused 2022 after losses) or Visor/Gamma's actively-managed V3 strategies that hedge dynamically; (4) Use options-based AMMs like Panoptic or Smilee that pay LPs option premiums. All hedges cost money (option premiums, funding rates) and reduce upside. Most retail LPs don't hedge and simply accept IL as the cost of yield. Not financial advice.

What is the math derivation behind IL = 2*sqrt(p)/(1+p) - 1?

Start with constant-product invariant x * y = k, where x and y are token quantities. Initial state: x0 * y0 = k, with price P0 = y0/x0. After price change to P1, the AMM rebalances to x1 = sqrt(k/P1), y1 = sqrt(k*P1), preserving k but shifting reserves. Pool value at new price = x1*P1 + y1 = 2*sqrt(k*P1). Hold value (if you'd kept original x0, y0) = x0*P1 + y0 = sqrt(k/P0)*P1 + sqrt(k*P0). Ratio = 2*sqrt(k*P1) / (sqrt(k/P0)*P1 + sqrt(k*P0)) = 2*sqrt(P1/P0) / (P1/P0 + 1) = 2*sqrt(p)/(1+p) where p = P1/P0. IL = ratio - 1 (negative for any p != 1). The derivative is zero at p=1, confirming IL is minimized when prices don't change, and grows symmetrically for upward and downward price moves.

Common Impermanent Loss Examples

- 1.25x price change → 0.6% IL (50/50 pool)

- 1.50x price change → 2.0% IL (50/50 pool)

- 2x price change → 5.7% IL (50/50 pool)

- 3x price change → 13.4% IL (50/50 pool)

- 5x price change → 25.5% IL (50/50 pool)

- DCA Calculator

- Crypto Profit/Loss Calculator

- Impermanent Loss Calculator

- ENS Resolver

- Blockchain Timestamp Converter

- Keccak SHA3 Hasher

- ABI Encoder / Decoder

- Checksum Address Converter

- EVM Vanity Address Generator

- Lido Rewards Tracker

- APR to APY Converter

- Bitcoin Unit Converter

- EVM Transaction Decoder

- Staking Rewards Calculator

- Tokenomics Chart Builder

- BIP39 Mnemonic

- Crypto Address Validator

- Crypto Logo Library

- Ethereum Unit Converter

- Mnemonic to Address

- Solidity Function Selector

- Wallet Address Validator

- Stablecoin Yield Comparator